The traditional proxies for where credit markets are heading – the 10-year, the CPI print, the dot plot, the Fed minutes – still matter. But anyone relying on that signal set alone is reading half the room. The inputs that move rate sheets in 2026 have widened, and the framework most of us grew up with needs to expand with them.

If you want to handicap where rates, housing, and the mortgage market are actually heading over the next few weeks, you have to widen the aperture. A lot of the signal right now isn’t coming from the housing data at all. It’s coming from a shipping lane in the Persian Gulf, a toll system enforced at gunpoint in the Gulf, and the procedural reality that Congress has no legislative path to bail anyone out before July.

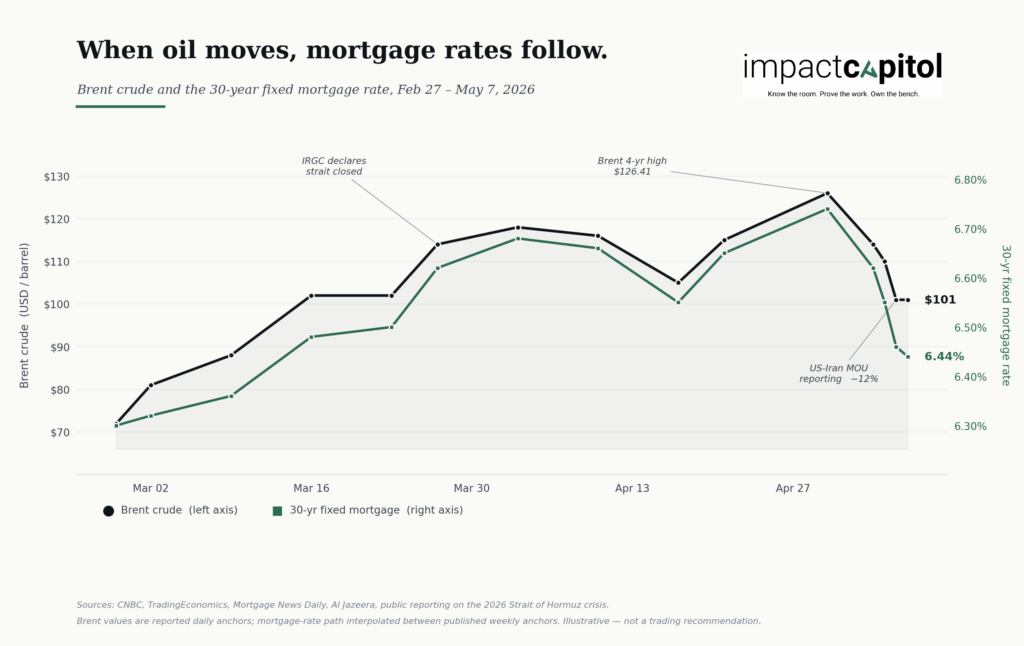

Here’s the chain. The Strait of Hormuz is still functionally closed. The IRGC has formalized a transit regime – roughly $1 per barrel, 20% fines for non-compliance, seizure risk if you don’t play ball. A 30-day partial reopening is on the table, widely read in DC as a US concession to keep next week’s Trump-Xi meeting on the rails. Now look at what oil did this week. Brent fell 12% Wednesday on reporting that a US-Iran memorandum was nearing completion, then stabilized near $101 today while Tehran ‘reviews’ the proposal. Every one of those headlines is moving the 10-year Treasury, and the 10-year is what your rate sheet tracks. The chart attached makes the relationship hard to miss.

Here’s the part I’d really focus on. Investors are starting to call around looking for stimulus – a payroll tax holiday, a federal gas tax suspension, anything to take pressure off consumers paying $4.50 a gallon and looking at $5 by Memorial Day. They’re not going to find it. Congress is on recess through May 12, and when they come back they have roughly eight working days before the next break. Those days are going to the second reconciliation bill of Trump’s term – about $70 billion to fund DHS and ICE through 2029. The tax-writing committees were not asked to participate. Translation: there is no legislative vehicle for stimulus, no gas-tax suspension, no payroll holiday in this bill. Anyone hoping Congress rescues the consumer before the midterms is reading the calendar wrong.

Which means any consumer relief between now and July is going to come from the executive branch – a 90-day federal gas tax suspension is on the table, and if pump prices touch $5, export controls on refined products move into the conversation. Meanwhile, the political read on Capitol Hill is that the President can simply ‘declare victory’ in Iran and end this. Maybe. But declaring victory doesn’t reopen the Strait, doesn’t resolve the IRGC tax problem, and doesn’t get cargo moving again. Politicians are focused on political dynamics. Markets are focused on commodity dynamics. That gap is where mispricing lives.

If you know where to look and what to look for, you get a head start on where rates and housing are heading. If you don’t, you’re reading about it after it’s already in your rate sheet. That’s most of what we cover in the Daily Dose of Real Estate – fastest growing newsletter in mortgage and real estate with 10k daily readers.. Sign up here https://impactcapitoldc.com/#signup